How To Remove paid (and unpaid) Collections From Your Credit Report

What is a collection account?

A collection account is created when your lender or creditor sells your debt to a third-party collection agency.

When you have an account that you have fallen behind on with payments or have stopped making payments altogether with your creditor, your creditor essentially gives up on trying to get payment from you and transfers your account to a collection agency or debt buyer.

This usually takes at least a couple of months of you being behind or late for your creditor will take this action.

What impact will a collection account have on my credit score and creditworthiness?

Having a debt in collections can really hurt your credit score

Having a debt in collections can really hurt your credit score

Unfortunately, if you are falling behind and struggling to make your payments on a credit card account or loan and the lender put your debt out for collections it will have a devastating short-term effect on your credit score.

Initially, when a collection first posts on your credit file, your score will probably drop over 100 points or more.

Over time, the negative impact of your collection account will diminish. After about 6 months your score can start to rebound as long as you are paying all of your bills on time and you do not have any other new derogatory information being posted to the credit bureaus.

In a few years, you will probably be able to get an auto loan, credit card, or mortgage but you will surely get higher interest rates as you will still not be deemed as the most trustworthy qualified buyer.

Getting the collection account removed and fixing your bad credit as soon as possible would be the best way to recover from a collection account.

Why did my paid collection remain on my credit report?

Unfortunately, if you did not negotiate a pay for delete when you made your payment with the collection agency or you did not set up some other sort of arrangement to have collection removed when you made your payment, the collection accounts whether they are paid or not will usually stay on your credit report for seven years. The seven years start from the actual date when you missed your first payment.

The good news is that there are a few strategies that you can try to have your paid collection removed from your credit report.

How Long Does A Collection Stay On Your Credit Report?

Collection accounts can remain on your credit report for around seven years after the date that the lender initially put your debt out for collections.

4 Strategies to Remove Paid Collections From Your Credit Report

These 4 strategies may help you to get your paid collections removed from your credit report.

1. Request a goodwill deletion

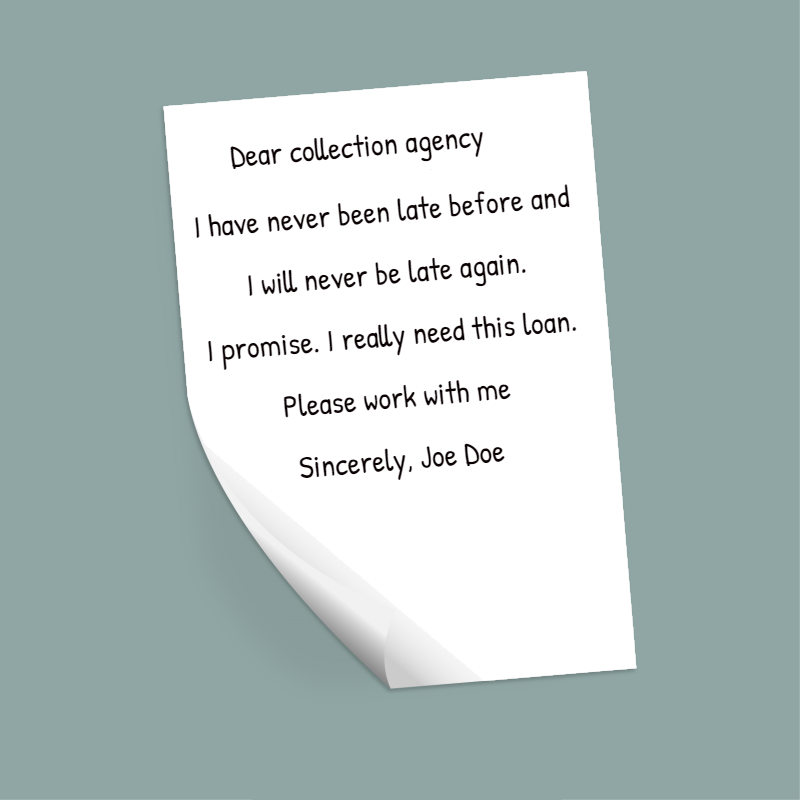

The first strategy that you should try is to send a “goodwill letter” to the collection agency to explain your situation. A goodwill letter essentially asks for forgiveness. When you’re asking for forgiveness give them a valid reason. If you were previously making payments on a regular basis and had no problems but then ran into small issues with making the payments, explain that to them.

Explain that you showed good faith in paying off the collection.

Tough times happen to good people. Explain to them that the negative item on your credit report is deterring you from getting a loan that you need or is hampering your chances of getting a mortgage that you are trying to get.

You are not necessarily trying to make them feel sorry for you, but you do want to state your case in a straightforward manner and asked them to remove the collections out of goodwill.

So with this first strategy, you simply want to (very nicely) ask the debt collector to remove your collection account out of goodwill.

If you are not sure how to write a goodwill letter, fear not! We have created an easy-to-read guide (complete with sample templates) on how to write a successful goodwill letter.

- 2. Dispute the collection

If your goodwill letter is unsuccessful and the debt collection remains on your credit report, then you could try disputing the collection with the three major credit bureaus.

The technique here is to find information that is not 100% accurate. Step one would be to get all three of your credit reports from all of the three major credit bureaus.

What you want to do is see if there are any discrepancies with the negative item in question across all three major credit bureaus. If say the amount you owe is different on all three credit bureaus, then you can dispute that the information is inaccurate and it must be removed from your credit. Check out this link 13 clever ways to raise your credit score and read tip number 6 very closely to see how to execute this strategy.

The FCRA (Fair Credit Reporting Act) mandates that the information being reported about you from the three major credit agencies must be 100% accurate. That is the loophole for this strategy to work.

This method will definitely work if you write an advanced in-depth dispute letter proving any discrepancies or inaccuracies.

If the balances owed are not identical across all three credit bureaus and that proves that at least one of them is wrong. Other inaccuracies to check for are the date that you opened and closed your account, the account number account, the date of the delinquency, your credit limit, and even payment history.

You want to look for anything at all that is not 100% correct. If you find anything at all you can dispute it and by law, they need to remove it.

If you cannot find any discrepancies across all three major credit bureaus pertaining to do your specific collection account.

Move on to the next strategy of asking the credit agencies to validate your debt.

- 3. Ask the collection agencies to validate the debt

Under the Fair Debt Collection Act, credit agencies are required to validate the debts that they are trying to collect on.

You have a legal right to ask the debt collection company to provide proof that the debt in question is actually yours.

They must also prove that they have the right to try to collect on a debt of yours on the behalf of the original creditor.

You can elude to your request for validation being made pursuant to 15 USC 1692g Sec. 809 (b) of the FDCPA.

Here is a great sample debt validation letter template.

Remember, the law for collection agencies to validate your debt was created for your protection as a consumer.

If the collection agency is unable to validate your debt, by law, they simply must remove it from your credit report.

- 4. Negotiate a pay-for-delete agreement

When your original creditor is unable to get a payment from you and they sell your debt collection agency, 9 times out of 10 they sell your debt for a deep discount.

Example:

Let’s assume that you owe $4,000 to your creditor and they cannot get a payment from you so they sell your debt to a collection agency for $500.

Your creditor doesn’t get the $4,000 that you owe them but they do get something; in this case $500.

In this scenario, you no longer owe your debt to your original creditor. You now owe it to the collection agency.

Then the debt collectors contact you and say hey you owe $4000. They are going to try to get the full amount in most cases.

But now that you know that they have paid for your debt for pennies on the dollar, you may have some leverage to negotiate.

The Negotiation for a pay-for-delete

You make an offer to pay $750 if they agree to remove any derogatory information that is existing on your credit report related to this account.

Have a professional credit repair company help you to remove collection accounts from your credit reports

Here is our #1 recommendation. Sky Blue Credit Repair.

How many points does your credit score go up when a collection is removed?

The answer to this question depends on a few different variables.

It depends on how old the collection is and how long it’s been reporting on your credit files. Other variables include how many other derogatory accounts that you have on your credit report and how many other collection accounts that you have.

But for the most part, your score can jump up anywhere between 25 and 150 points!

The less amount of other derogatory accounts that you have the higher your jump will be from deleting a collection account.

Collection Accounts FAQ’s

1. What is a collection account on your credit report?

A collection account is an account that shows up on your credit report when you fail to repay your original creditor. Your original creditor will sell your debt to a collection agency and that collection agency will immediately report the debt on your credit report and it will show up as a negative item.

2. Can you remove a collection account without paying it?

Yes, you can remove a collection account without paying the debt if you can prove that the information is not 100% accurate or if the collection agency cannot legally validate the debt.n get a free credit report every week because of the Covid-19 pandemic. So all you have to do is visit annualcreditreport.com to get your free credit report.

Final Thoughts

It is always a good idea to pay a collection account off if you have the money.

Absolutely always make sure to make an offer to pay down the collection if they agree to delete the negative collection account item off of your credit reports.

Even if you owe the debt, you can still get the items removed the information is not 100% accurate.

Consider hiring an experienced professional credit repair company like Sky Blue Credit Repair that will handle the entire process for you.

Related Reading

How to write an effective goodwill letter.

Does requesting a credit line increase hurt your score? See an easy-to-read answer to this question.

Does collecting unemployment affect your credit score?

See 5 credit repair laws and loopholes that you can use immediately to raise your score.

Learn the secrets on how t0 get an 800 FICO score.

Leave A Comment